When you receive your financial aid offer, you’ll notice that it is broken down into several key components. Here’s what they mean.

Estimated cost of attendance

The cost of attendance (COA) is our best estimate—based on defined costs set by MIT and surveys of our students—of what we expect it to cost you to attend MIT for one academic year as a full-time student.

When we award you financial aid, it is based on the assumptions of the COA. Whether you end up spending more or less than our estimate, your demonstrated financial need and financial aid offer stay the same.

Family financial responsibility

Our assessment of how much you and your parent(s) or guardian(s)01 We refer to parents and guardians as family, knowing that every situation is different. can reasonably be expected to contribute to the cost of your education for the upcoming academic year. It is composed of the parent contribution and the student contribution.

Parent contribution

The amount we believe your parent(s) or guardian(s) can reasonably be expected to contribute toward the cost of education for the upcoming year, based on the information provided to us. This is different for every family. We carefully review each application to make sure you receive the financial aid that is right for you.

Student contribution

The amount we believe you can reasonably be expected to contribute toward the cost of your own education by working over the summer and/or during the school year.02 You don’t have to contribute these amounts at these specific times, this is just what students often do. By default, this is set to $5,400, broken down into two components based on what our data and experience suggests students can reasonably do:

- Summer savings expectation: We set this to $2,000, the amount we expect you could reasonably contribute from income earned over the summer.

- Student employment: We set this to $3,400, the amount we expect you could reasonably contribute by working less than 10 hours per week during the academic year.

Grants and scholarships

Grants and scholarships are funds we (or other entities) are granting you.

Loans

We include a loan section on the offer to help you compare financial aid across schools, even though we do not expect you will need to take out any loans to pay for MIT. However, if you and your family are considering a loan to help manage your finances, we can help you with that.

Example aid offer

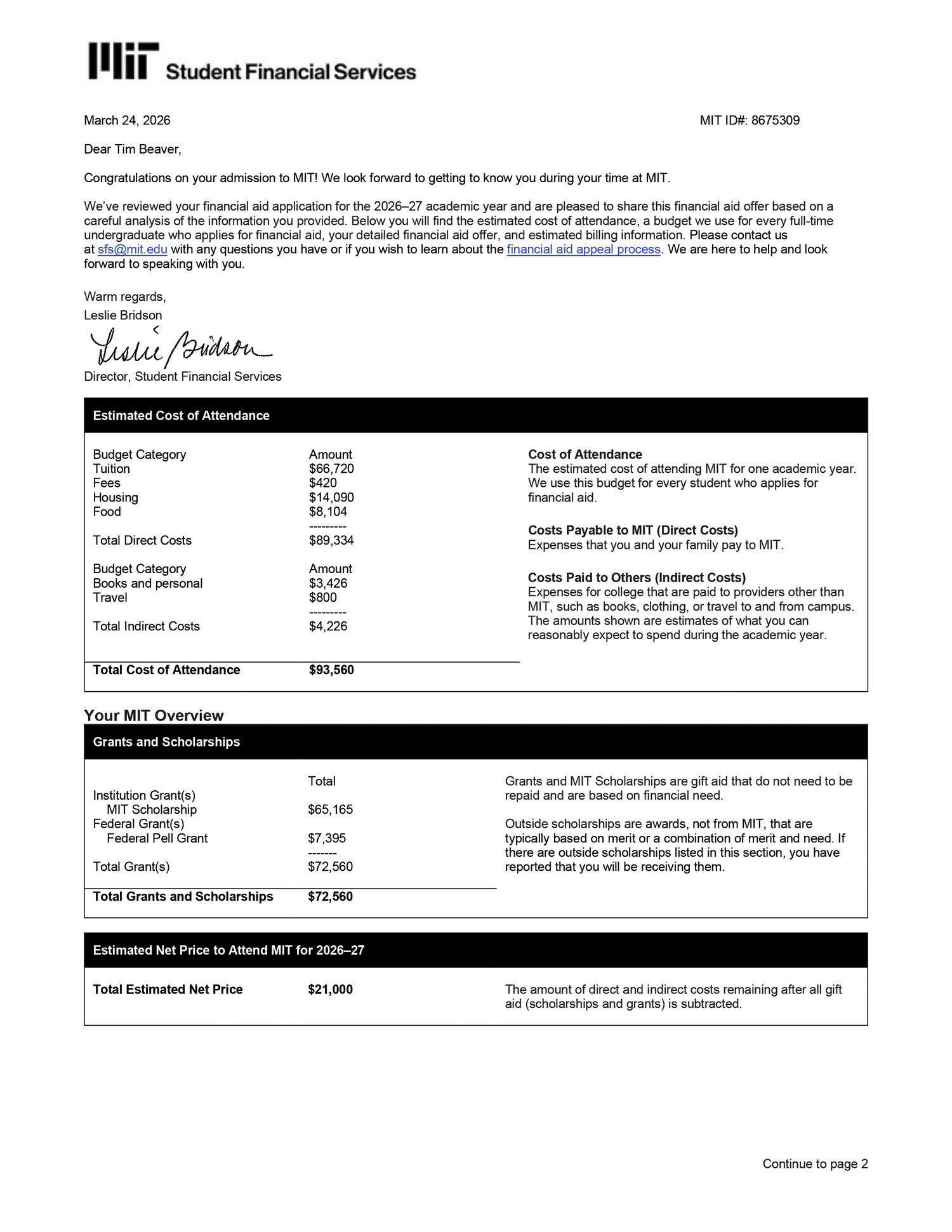

To help you understand what an aid offer might look like and how to interpret it, we have created an example financial aid offer for a fictional student, using figures and policies from 2026–2027.

Fictional first year Tim Beaver03 Tim Beaver is a fictional first year named after MIT’s mascot. Like humans, beavers tend to live in groups called families that work hard and mutually help each other. While this is not always true for all beaver or human families, it is a starting (but not ending) point for our analysis. has filled out the FAFSA, which has determined they qualify for a full Federal Pell Grant of $7,395. That Pell Grant, as an outside scholarship, first reduces Tim’s student contribution to zero, so Tim has no work expectation.04 However, being characteristically industrious, Tim may still choose to work, and retain the products of that labor without changing this aid expectation.

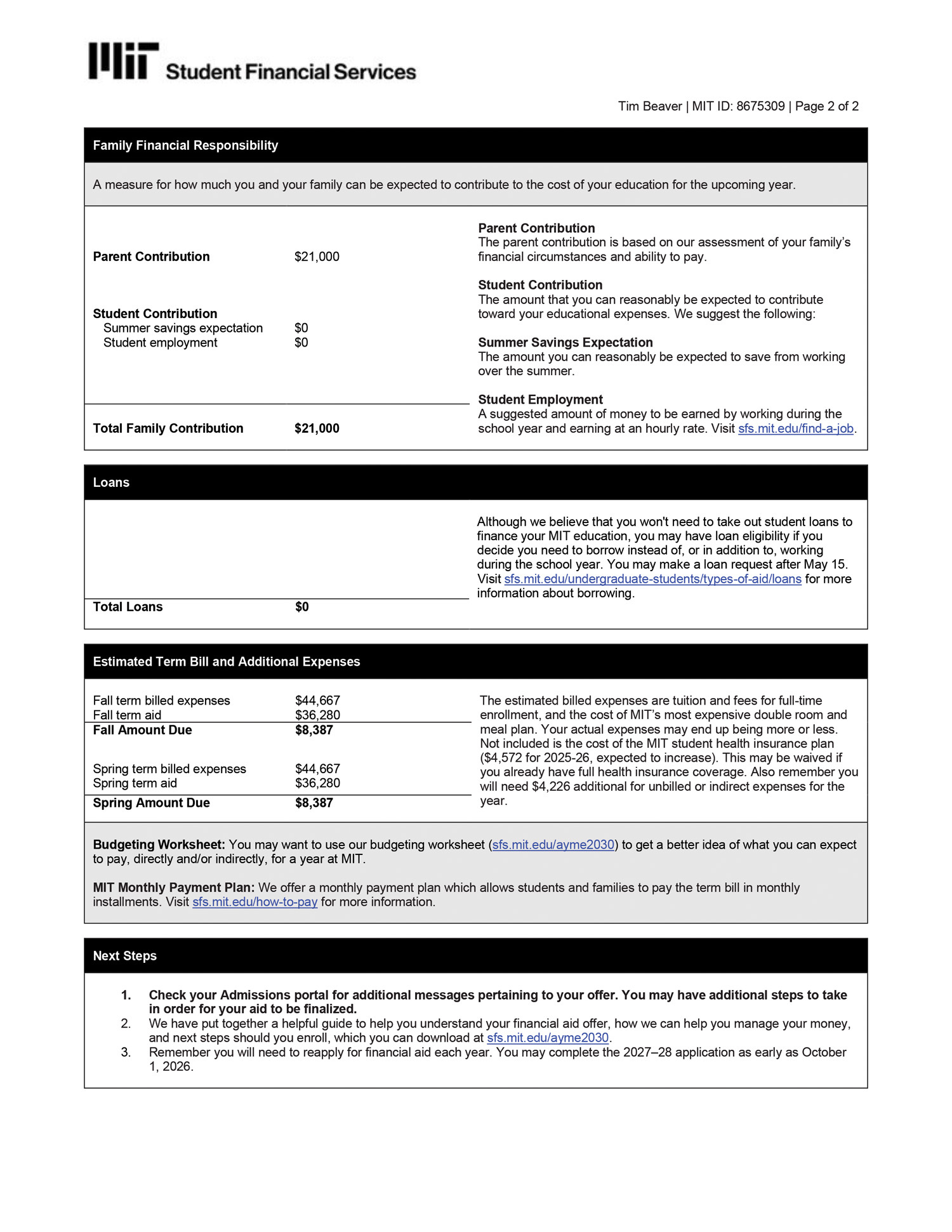

Our need analysis has further determined that Tim and their family can afford to contribute $21,000 per year toward their MIT education. The difference between the COA ($93,560) and their family financial responsibility ($21,000)05 In this case, the outside scholarship has reduced the student contribution of the family financial responsibility to zero, so there is only a parent contribution. Every case is different. is made up by the MIT Scholarship ($65,165), a grant from MIT to Tim and their family that does not need to be repaid.

The bottom of the letter reports the estimated term bill, split into fall and spring terms, net of financial aid. In this case, MIT expects to directly bill Tim (and their family) $8,387 per term.

Because Tim’s mind is as sharp as their incisors, they notice that this sums to $16,774—which is $4,226 less than the $21,000 listed in the family financial responsibility.

This difference captures the indirect costs not billed to MIT: books, personal expenses, and transportation to campus. MIT has estimated that Tim may need to budget $4,226 to buy these things; however, if Tim spends more or less, it doesn’t raise or lower the MIT Scholarship, Pell Grant, or other sources of aid. Tim and their family resolve to plan these purchases carefully, further reducing their actual costs to attend MIT.

- We refer to parents and guardians as family, knowing that every situation is different. back to text ↑

- You don’t have to contribute these amounts at these specific times, this is just what students often do. back to text ↑

- Tim Beaver is a fictional first year named after MIT’s mascot. Like humans, beavers tend to live in groups called families that work hard and mutually help each other. While this is not always true for all beaver or human families, it is a starting (but not ending) point for our analysis. back to text ↑

- However, being characteristically industrious, Tim may still choose to work, and retain the products of that labor without changing this aid expectation. back to text ↑

- In this case, the outside scholarship has reduced the student contribution of the family financial responsibility to zero, so there is only a parent contribution. Every case is different. back to text ↑