Our mission is to ensure an MIT education is affordable to every admitted student on the basis of their talent, regardless of their financial circumstances.

Upon admission, every MIT student is assigned to a financial aid counselor.01 Counselors are assigned by the first letter of your last name—feel free to reach out to your counselor with any questions you may have. Your counselor works carefully to understand your financial situation in order to assess need and award aid equitably.

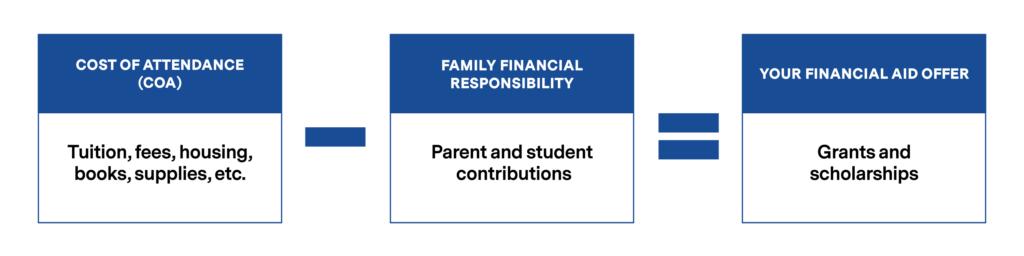

Every family has specific, personal circumstances, but this is our general process:

- We estimate your cost of attendance (COA), or how much we expect MIT to cost for you to attend for the current academic year.

- We review your financial aid forms to establish your family financial responsibility, or how much we believe you and your family can be reasonably expected to contribute toward your MIT education. To do this, we apply a consistent approach known as “need analysis” to every family’s unique circumstances.

The difference between the COA and family financial responsibility is how we calculate what we will award you in institutional grants and scholarships.

How we conduct need analysis

“Need analysis” is the term used in our profession to refer to our process of determining how much you and your family can afford to pay for MIT, and thus your “demonstrated financial need” that must be met with aid. As we described above, this process is both highly individualized to the specific circumstances of each family, while the principles apply consistently across families. This is how we attempt to ensure both affordability and fairness for all of our undergraduates.

Like the admissions process you’ve just experienced, this process is run by dedicated professionals with a commitment to our mission of helping every admitted student afford MIT. Each application is read by two financial aid officers to help ensure consistency and impartiality across cases.

In order to conduct a need analysis, we require extensive financial information from your parent(s) or guardian(s), whether custodial and/or noncustodial.02 A term used in connection with separated and divorced parents to refer to the parent who does not have custody of the child, or the parent with whom the child does not live with the majority of the time. If, however, there are extenuating circumstances that prevent noncustodial parent information from being provided, you may request a waiver of the noncustodial parent’s information.

Because of the complex and individualized nature of our need analysis, it is impossible to list all of the considerations that determine your financial aid. However, at a high level, our counselors evaluate demonstrated need by using two frameworks:

- The Free Application for Federal Student Aid (FAFSA)

- The College Board’s Institutional Methodology,03 A research-backed measure of family financial strength. which we highly customize to align with MIT’s principles of affordability

People often ask what we consider at a more granular level. An incomplete list of factors we consider when assessing ability to pay includes:

- Number of people in the family

- Number of children currently attending college as an undergraduate

- Country/state of primary residence

- Total parent income04 MIT defines total family income as income from all sources, taxable and non-taxable. It can include, but is not limited to, wages from work, business and real estate income, self-employment income, unemployment compensation, child support, and alimony, as well as contributions to, and distributions from, retirement accounts. from all sources, whether taxed or untaxed

- Taxes paid

- Non-reimbursed medical expenses

- Private school tuition for younger siblings

- Total assets05 Cash, non-retirement investments, real estate (excluding your primary home), the value of businesses, etc.

However, we cannot emphasize enough the highly individualized nature of this approach. If, after we have offered you aid, you believe that we have misunderstood something about your family’s financial situation, you may request a review and share more information.

Still have questions?

If you have any questions about your financial aid, or if you need our help navigating a complicated situation, please contact us! We want to understand the complexities of your financial situation and do our best to make your MIT education affordable.

- Counselors are assigned by the first letter of your last name—feel free to reach out to your counselor with any questions you may have. back to text ↑

- A term used in connection with separated and divorced parents to refer to the parent who does not have custody of the child, or the parent with whom the child does not live with the majority of the time. If, however, there are extenuating circumstances that prevent noncustodial parent information from being provided, you may request a waiver of the noncustodial parent’s information. back to text ↑

- A research-backed measure of family financial strength. back to text ↑

- MIT defines total family income as income from all sources, taxable and non-taxable. It can include, but is not limited to, wages from work, business and real estate income, self-employment income, unemployment compensation, child support, and alimony, as well as contributions to, and distributions from, retirement accounts. back to text ↑

- Cash, non-retirement investments, real estate (excluding your primary home), the value of businesses, etc. back to text ↑